Is It Better to Pay Off House or Car First? 7 Expert Tips

Are you grappling with the financial puzzle of is it better to pay off house or car first? It’s a common question for many, and understanding the best approach can significantly impact your financial well-being. Deciding whether to prioritize your mortgage or your car loan can feel overwhelming, but with the right information, you can make a choice that aligns with your financial goals.

Understanding the Debt Dilemma: Car Loan vs. Mortgage

When you’re juggling multiple debts, figuring out where to focus your extra funds can be tricky. Many people find themselves wondering should i pay off my car before buying a house, or perhaps they already own a home and are debating pay off car loan before buying house. The truth is, there’s no one-size-fits-all answer to pay off car or mortgage first. The optimal strategy depends on your individual circumstances, financial priorities, and risk tolerance.

Let’s break down the two main types of debt we’re discussing:

- Car Loans: Typically, car loans are shorter-term debts, often ranging from 3 to 7 years. They usually come with higher interest rates compared to mortgages, especially for those with less-than-perfect credit scores. The value of a car also depreciates over time, meaning the asset securing the loan loses value. A monthly car payment can be a significant drain on your gross monthly income.

- Mortgages: Home loans, or mortgages, are long-term debts, typically spanning 15 to 30 years. Historically, they have lower interest rates than auto loans, although this can fluctuate with market conditions. Unlike cars, homes generally appreciate in value over time, making them an appreciating asset. Securing a mortgage application and getting approved for a home loan is a major financial undertaking.

The Case for Paying Off Your Car First: Quick Wins and Financial Flexibility

For some, the best approach is to focus on paying off your car before tackling the mortgage. Here’s why this strategy might be appealing:

- Higher Interest Rates: As mentioned, car loans often carry higher interest rates than mortgages. By eliminating this debt first, you can save a significant amount of money on interest payments over the life of the loan. Every dollar saved on interest is a dollar you can redirect towards other financial goals, including your mortgage.

- Faster Debt Reduction: Because car loans are typically shorter-term, you can see progress much faster when you prioritize them. The psychological boost of paying off a car relatively quickly can be incredibly motivating. This quick win can provide momentum and encourage you to tackle larger debts like your mortgage with renewed enthusiasm.

- Improved Cash Flow: Eliminating your monthly car payment frees up cash flow immediately. This extra money can be used to accelerate your mortgage payoff, build an emergency fund, invest, or pursue other financial goals. Having more disposable income provides greater financial flexibility and reduces financial stress.

- Better Debt-to-Income Ratio: Lenders look at your debt to income ratio (DTI) when you applying for a mortgage or refinancing. This ratio compares your monthly debt payments to your gross monthly income. Paying off your car reduces your monthly debt payments, thereby improving your DTI. A lower DTI makes you a more attractive borrower to mortgage lenders and can improve your ability to qualify for a home loan or better mortgage terms in the future. Even if you already own a home, a better DTI can be beneficial for future financial endeavors.

- Reduced Financial Risk: Cars depreciate. If you face financial hardship and need to sell your car, you might find yourself owing more on the loan than the car is worth. Paying off your car eliminates this risk. Furthermore, having one less debt hanging over your head can reduce overall financial anxiety.

For example, imagine you have a$20,000 car loan at 7% interest and a$200,000 mortgage at 4% interest. While the mortgage is a larger debt, the higher interest rate on the car loan means you’re paying more proportionally in interest each month on the car. Paying off your car first would save you more in interest in the short term and free up cash to then aggressively pay down the mortgage.

The Case for Paying Off Your House First: Long-Term Security and Wealth Building

On the other hand, prioritizing your mortgage and aiming to pay off your mortgage first also has compelling advantages:

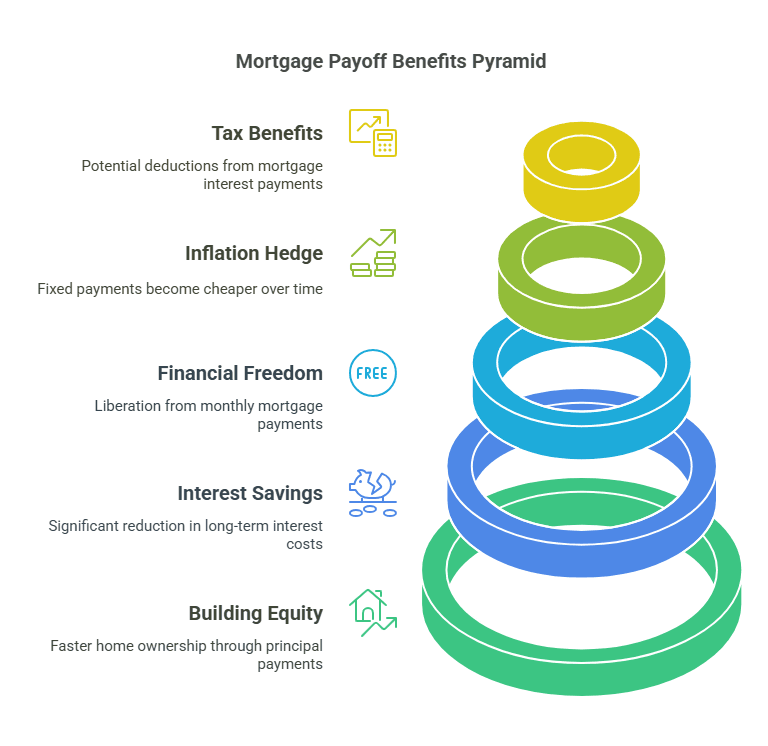

- Building Equity Faster: Every mortgage payment you make is split between principal and interest. In the early years of a mortgage, a larger portion of your payment goes towards interest. By making extra payments towards the principal, you can build equity in your home faster. This increased equity strengthens your financial foundation and provides a sense of long-term security.

- Long-Term Interest Savings: While mortgage interest rates are typically lower than car loan rates, the sheer size and duration of a mortgage mean you’ll pay significantly more in total interest over the life of the loan. Even a slightly lower interest rate applied to a much larger principal over 30 years accumulates to a substantial sum. Paying off your mortgage first, or at least aggressively paying it down, can save you tens or even hundreds of thousands of dollars in interest over the long run.

- Future Financial Freedom: Imagine life without a monthly mortgage payment. This is the reality of paying off your house. The freedom from this significant monthly expense can be transformative. It opens up opportunities to retire earlier, pursue passions, travel, or simply have more financial breathing room. This long-term financial freedom is a powerful motivator for prioritizing mortgage payoff.

- Inflation Hedge: Mortgages often have fixed interest rates. As inflation rises, your fixed mortgage payment becomes relatively cheaper over time in today’s dollars. While inflation also affects other expenses, having a fixed housing cost can provide stability in an inflationary environment. Focusing on paying off a fixed-rate mortgage can be seen as a way to lock in today’s dollars for a long-term expense.

- Potential Tax Benefits: In some regions, mortgage interest is tax-deductible (though this can be subject to limitations and changes in tax laws). While this shouldn’t be the primary driver of your decision, it’s a potential benefit to consider. However, it’s crucial to consult with a tax advisor to understand the specific tax implications in your situation.

Consider this scenario: You have the same$20,000 car loan at 7% and a$200,000 mortgage at 4%. While paying off your car provides a quicker sense of accomplishment, focusing extra payments on the mortgage, even small amounts consistently, will drastically reduce the total interest paid over 30 years. This long-term saving can be more impactful for your overall wealth accumulation.

Key Factors to Consider: Making the Right Choice for You

Ultimately, the decision of is it better to pay off house or car first is personal. Here are some crucial factors to weigh when making your choice:

- Interest Rates: Compare the interest rate on your car loan to your mortgage rate. If your car loan has a significantly higher interest rate, prioritizing it might save you more money in the short term. However, consider the total interest paid over the life of each loan.

- Loan Balances and Terms: Look at the outstanding balances and remaining terms of both loans. A smaller car loan with a shorter term might be quicker to eliminate, providing that psychological boost. A larger mortgage with a longer term will require a more sustained effort but offers significant long-term savings.

- Financial Goals and Priorities: What are your immediate and long-term financial goals? Are you planning to buy a home soon? Improving your credit score and DTI by paying off your car might be beneficial for applying for a mortgage. Are you focused on long-term wealth building and financial independence? Aggressively tackling your mortgage might align better with these goals.

- Risk Tolerance: How comfortable are you with debt? Some people prefer the peace of mind of eliminating smaller debts quickly, even if the long-term interest savings might be greater with the mortgage. Others are more focused on maximizing long-term wealth and are comfortable with a longer debt payoff journey for the mortgage.

- Credit Score Impact: Paying off a car loan can have a slight positive impact on your credit score by reducing your overall debt burden. However, the impact is usually less significant than consistently making on-time payments. Focus on responsible credit management overall, including timely payments on all debts and keeping credit card debt in check. You can check your credit reports regularly to monitor your credit health.

- Personal Financial Situation: Consider your current income, expenses, and emergency savings. If you have limited savings, paying off your car and freeing up cash flow might provide a safety net. If you have a comfortable emergency fund, you might be more comfortable directing extra funds towards your mortgage.

Making Your Decision and Taking Action

There’s no right or wrong answer to is it better to pay off house or car first. The best approach is the one that aligns with your individual financial situation, goals, and priorities. Carefully evaluate the factors discussed above, and consider consulting with a financial advisor for personalized guidance.

Once you’ve made your decision, create a plan and take action. Whether you choose to attack your car loan or your mortgage first, consistency is key. Even small extra payments made regularly can make a significant difference over time. Consider setting up automatic extra payments to stay on track.

Remember, managing debt effectively is a crucial step towards financial well-being. By thoughtfully considering your options and making informed decisions about paying off your car versus your mortgage, you can pave the way for a more secure and prosperous financial future.

Let me know if you would like any adjustments or further refinements to this article!

There are no reviews yet. Be the first one to write one.